Financial professionals generally describe an index decline of 10% or more from a market peak as a “correction”. The age old question – “after a 10% decline, should investors seek to protect themselves from further decline by selling, or should they consider it an opportunity to purchase stocks at the lower prices currently available” – is a question we discuss frequently with clients, and, a question that recent market volatility has brought to the collective attention of investors.

As most investors know, stock prices in markets around the world fluctuated dramatically in August. On Monday, August 24th, the Dow Jones Industrial Average fell 1,089 points—a larger loss than the “Flash Crash” in May 20101 before rallying to close down 5882. Prices fell further on Tuesday before recovering sharply on Wednesday, Thursday, and Friday. Although the S&P 500 and Dow Jones Industrial Average rose 0.9% and 1.1%, respectively for the week, many investors found the dramatic day-to-day fluctuations unsettling. While the Dow was gyrating the S&P 500 also vacillated – based on closing prices, the S&P 500 Index declined 12.35% from its record high of 2130.82 on May 21st through August 24th.

Contrary to the beliefs of many investors and most market pundits, dramatic changes in security prices are not a sign that the financial system is broken but rather – precisely what we want and expect to see when markets are working properly – Buyers and Sellers are Trading Freely!

The role of securities markets is to reflect new developments – both positive and negative – in security prices as quickly as possible. Investors who accept dramatic price fluctuations as a characteristic of liquid markets may have a distinct advantage over those who are easily “frightened or confused” by day-to-day events! We believe investors who accept the collective wisdom of market participants in establishing security prices and accept those prices as “fair” are more likely to achieve long-term investing success than those investors who believe that freely traded highly-liquid securities are priced “unfairly”.

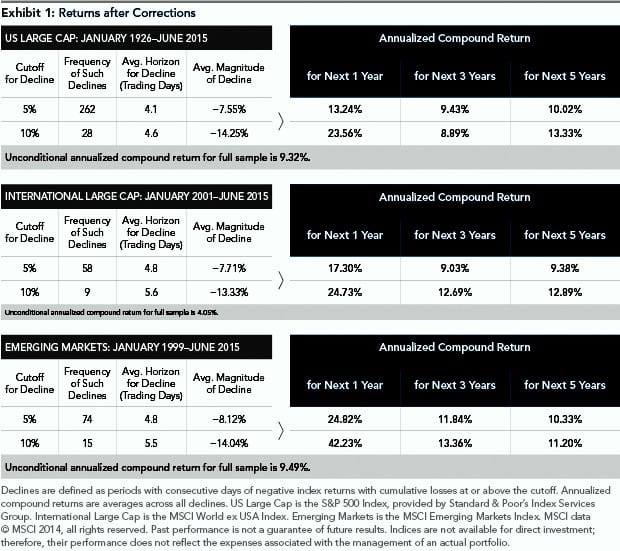

Based on S&P 500 data, stock prices have declined 10% or more on 28 occasions between January 1926 and June 2015 – about once every three years. Obviously, every decline of 20% or 30% or 40% began with a decline of 10%. As a result, some investors believe that avoiding large losses can be accomplished by eliminating equity exposure (selling stocks) entirely once the 10% threshold has been breached. Is this “drawdown driven selling” really a good strategy? This strategy is Market Timing and begs the question “Do You Believe In Market Timing”?

Market timing is seductive. If we could sell stocks prior to a substantial decline, hold cash until just the right moment, then, “pounce” and buy at the new bottom, our long-term returns would be exponentially higher. As pointed out above, the successful market timer would have to make two correct decisions every few years. Over an investor’s lifetime of give-or-take forty years – this would require Twenty-Six Sequentially Correct Decisions! Lots of clairvoyance required!

In the words of industry veteran Peter Lynch:

“I Don’t Remember Anybody Predicting The Market Right More Than Once…

And They Predict A Lot.”

The razor blade in the pudding of “drawdown driven selling” is that “attempting to avoid further short-term losses via selling risks missing even larger long-term gains”.

Exhibit 1 below shows that US and Non-US Stocks Have Typically Delivered Above-Average Returns over the One, Three and Five Year Periods Following Consecutive Negative Return Days That Resulted in A 10% Or Greater Decline:

Let us admit to ourselves that regardless of whether stock prices have advanced 10% or declined 10% from a previous level, current prices always reflect:

- The Collective Assessment Of The Future By Millions Of Market Participants And

- Investors In The Marketplace Have Priced Securities At Levels Whereat They Expect Returns In Both US And Markets Around The World To Be Attractive In The Future.

Toward removing “fright and confusion” and Not Letting Emotions Influence Investing Decisions, we recommend developing realistic expectations, turning off the financial press, turning on objective academic evidence and Developing A Purposeful Plan. A Purposeful Plan should provide future access to currency for lifestyle while insulating exposure to risky/volatile assets such that you are less likely to need to sell risky/volatile assets in one of the many inevitable corrections yet to come.

To answer the “time to buy or sell” question posed in the opening paragraph:

- Investors With A Purposeful Plan In Place Should Probably Do Nothing…Unless…Their Personal Situation Has Changed.

- Investors With No Plan In Place Should Derive A Purposeful Plan! Absent A Purposeful Plan For Guidance – Neither I Nor Anybody Else Knows What To Advise.

- Investors With Substantial Resources Might Consider Buying More. Why? Because History Shows Us – (See Exhibit 1) – That Market Returns After A Correction Have Historically Been Greater Than Normal. (No Guarantees!)

Inviting the opportunity to have dialogue with you and hoping you will find this missive to be interesting/useful as you pursue the achievement of your Wealth Management Goals, I remain

Yours truly,

Warburton Capital Management

Data is from sources deemed to be reliable but not guaranteed.

References:

1 “Wild Ride Leaves Investors Grasping,” Wall Street Journal, August 25, 2015.

2 “Investors Scramble as Stocks Swing,” Wall Street Journal, August 25, 2015